Efficient and Accurate Information Disclosure applying Data Quality Principles

In this article Asset Dynamics’ Andrew Gatland and Jules Congalton outline a proven methodology for accurate and efficiently meeting Information Disclosure requirements.

Role of Information Disclosure

Information Disclosure is one of the tools used by the New Zealand Commerce Commission to regulate utility businesses including electricity distributors, gas pipeline businesses, fibre network providers, and soon, water network operators. Businesses that are subject to information disclosure regulation must publish information each year detailing their performance.

Information Disclosure is an effective regulatory tool as it establishes a consistent data standard for capturing and reporting information, makes performance information transparent, enables benchmarking across suppliers, and allows performance trends to be tracked over time.

Regulated suppliers must disclose a range of information including asset management plans, capital and operating expenditure forecasts, asset condition information, capacity and demand forecasts, reliability forecasts, and asset management maturity self-assessments. This can be a significant demand on internal resources. By treating Information Disclosure as a critical business capability and developing efficient processes and systems, regulated businesses can minimise the long-term cost of meeting these requirements and manage down exposure to the risk of penalties for errors.

In this article we provide an overview of an approach to meeting Information Disclosure Requirements for quantitative information which has been implemented successfully in multiple electricity distributors. This approach links information disclosure requirements with information held in asset management information systems and establishes automated data quality checks that can be applied consistently to ensure data are of appropriate quality.

Such an approach is preferable to waiting to the end of the Regulatory Year before verifying information for disclosure, as any data quality issues introduced during the period will need to be addressed in a reactive fashion, creating the risk of further errors.

Information Requirements

Precisely defining asset information requirements is fundamental to successful asset information management. Infrastructure organisations require asset management data and information for a wide range of purposes including asset planning and decision-making, tactical and operational planning, delivering work, evaluating performance, and financial and non-financial reporting to stakeholders. In many cases the same data is required for multiple purposes, for example asset condition information may be used for assessing asset risk and therefore renewal priority, confirming equipment is safe to operate, and reporting to stakeholders.

Information requirements associated with Information Disclosure should be treated no differently to other information requirements and will in many cases point to a high criticality data asset due to the compliance imperative.

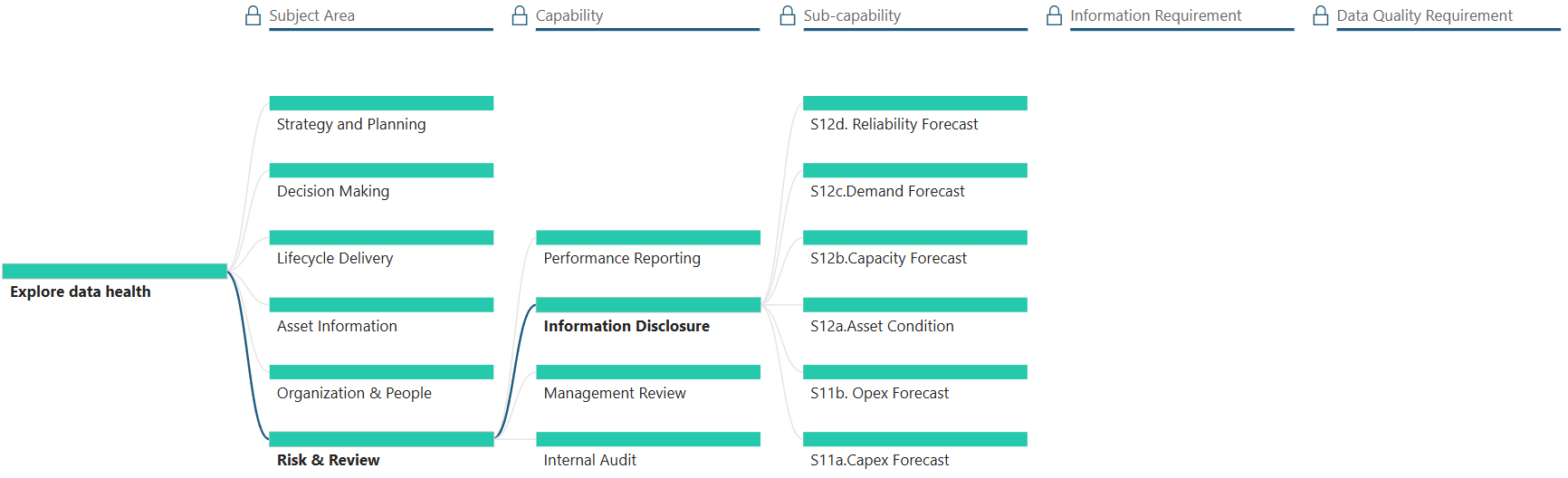

Information requirements may be presented as a hierarchy organised under the major asset management Subject Areas and Capabilities that consume data. Figure 1 shows an example of a breakdown of the key asset management Subject Areas that consume data in an electricity distribution business. The Information Disclosure Capability is shown as belonging to the “Risk & Review” Subject Area. The “Information Disclosure” Capability has six Sub-capabilities which represent the business capability to complete six asset management related Information Disclosure Schedules.

Figure 1: Information Disclosure Schedules within the Asset Management System

Schedule 12a: Report on Asset Condition requires a breakdown of asset condition by asset class as at the start of the forecast year. The data accuracy assessment relates to the percentage values disclosed in the asset condition columns. Also required is a forecast of the percentage of units to be replaced in the next 5 years. This Schedule is partially reproduced in Figure 2.

Figure 2: Electricity Distribution Information Disclosure Requirements Schedule 12a: Report on Asset Condition (partial reproduction)

The fields of Schedule 12a are represented as Information Requirements under the “S12.a Asset Condition” Capability shown in Figure 3. These include condition ratings, data accuracy grades, and asset replacement forecasts for each Asset Category. Each of these Information Requirements must be associated with a field or fields in the source asset management information system, for example Enterprise Asset Management System (EAMS) or Geographic Information System (GIS).

Figure 3: Information Requirements to complete Schedule 12a: Report on Asset Condition

Data Quality Requirements

Once the Information Requirements have been identified, applicable Data Quality Requirements can be determined. Data Quality Requirements are specific algorithmic checks to be performed against the data to confirm its fitness for purpose or otherwise. These checks will typically be based on data quality dimensions such as those shown in Figure 4.

Figure 4: Data Quality Dimensions

Four Data Quality Requirements have been defined for Underground Cable Condition data.

“Complete” checks that the condition data is complete, or in other words, 100% of cable segments have a value entered in the Commerce_Commission_Condition field within the EAMS.

“Valid” checks that 100% of cable segment condition data is valid, i.e., has a value of “H1” to “H5” or “Unknown”.

“Consistent” checks that the average condition grade of the fleet has not changed by greater than a certain threshold compared to what was disclosed in the previous period.

“Percent Unknown” checks that the number of cable segments with condition “Unknown” has not increased since the last period which could indicate an error, as current installation and condition assessment processes require that a condition grade is provided.

A range of data quality checks may be established depending on what is appropriate for the Information Requirement. The four Data Quality Requirements for Underground Cable Condition are shown in Figure 5.

Figure 5: Data Quality Requirements

With the Data Quality Requirements established and implemented as queries across the relevant data, it is possible to report on data quality. Figure 6 shows an 'amber' check against the “Consistent” data quality requirement. This indicates that the condition data for underground cables should be checked to confirm that the change since the previous reporting period is accurate. It is possible that an error has been introduced, however such a change could also have resulted from the implementation of a proactive cable testing programme resulting in improved asset condition information for this fleet since the last reporting period.

Figure 6: Data Quality Checks

A clear perspective on data quality for each Information Disclosure schedule can be produced in this way. If data quality issues are monitored continuously to address errors and underlying root causes of data quality problems, then producing quantitative information becomes a straightforward, efficient, and low cost process.

Conclusion

The Commerce Commission’s Information Disclosure approach continues to expand its breadth within existing regulated sectors and will soon apply to water services operators. Regulated businesses should treat Information Disclosure as a critical business capability and develop efficient processes and systems to minimise the long-term cost of meeting these requirements and manage down exposure to the risk of penalties for incorrect disclosure.

This article has provided a structured approach to establishing control on asset data and information that has proven to be effective for managing Information Disclosure obligations. By maintaining regular reporting of data quality associated with Information Disclosure obligations errors can be corrected as they arise, and the root causes of errors can be pinpointed and addressed.

Contact Us

Thank you for reading. If you have any questions on this article or would like tailored advice on this topic, please complete the form below and we will be in touch as soon as possible.